Does Lyft Notify your Insurance When you Start Driving?

Driving apps like Lyft and Uber have changed the way we travel around our cities. They have shaken up the taxi monopoly and challenged the status quo of public transit or cab and now offer a third way. These apps also offer employment opportunities for those with a decent car who want to earn a little money. If you’re one of these drivers, does Lyft notify your insurance when you start driving?

Insurance is a key part of driving wherever in the world you live. If you drive for a living or carry paying passengers, insurance is even more important. The last thing you want is not to be covered when you need it most or face a lawsuit from an unhappy or injured passenger. So what insurance do you need? Does Lyft tell your insurer when you begin driving for them?

Before we begin, it is impossible to offer exact information for every insurance type or provider out there. Use this as a general guide and make sure to consult your insurance company for specific guidance. Lyft’s insurance is explained on this page.

Will your current insurance cover you driving for Lyft?

If you’re like most of us who drive, you will have personal insurance that covers you for most situations you find yourself in on the road. It will not cover you for driving for Lyft unless you have a specific ride-share feature on your policy. If you don’t have this feature, you don’t have cover.

Personal car insurance does not cover you when you drive for reward, i.e. when carrying paying passengers. If anything happens during that time, you have some coverage from Lyft but there are holes in that coverage. There are also steep deductibles to take into account.

Does Lyft notify your insurance company when you start driving?

Lyft does not currently notify insurance companies of individual drivers. It will check your state’s or country’s insurance database to make sure you have insurance but does not actively inform any insurer. That’s up to you.

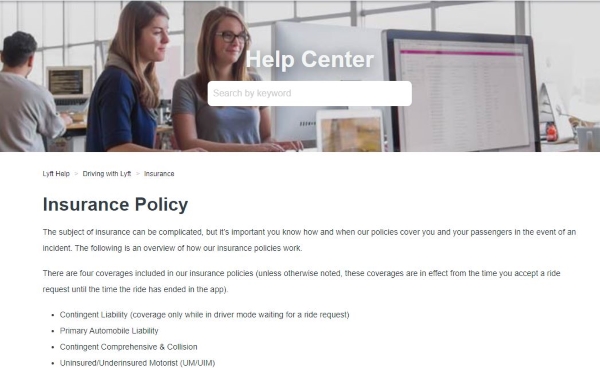

What does Lyft insurance cover and when?

Uber and Lyft both offer very similar insurance with similar restrictions and deductibles. They divide the ride up into periods and don’t cover them all. Here’s a basic outline of what’s covered and what isn’t.

When you’re not using the Lyft app

You’re not covered by Lyft insurance. You need to have the app active and be in one of the three stages of the ride to be covered. Only when you’re in ‘driver mode’ will you be covered.

When you’re logged into Lyft and waiting for a ride

If you’re logged into the Lyft app and are waiting for a request, you have some cover. That cover insures losses sustained by others but not you. That means any third party losses will be covered by the insurance but damage to you or your car is not covered.

When you’re on your way to a pickup

When you have accepted a ride request and you’re on your way to pick up your ride, you have cover of up to a $1 million for liability. This is restricted to third party liability again. That means if you hit someone, their car and injury is covered and your passenger is covered. You and your car are not.

During the ride

You have the same $1 million liability coverage during the ride as you do om your way to the pickup. It has the same restrictions too.

There are contingent cover options available that are explained on the Lyft website. It is designed to work alongside your own insurance to cover your own vehicle in the event of collision or damage.

About those deductibles

Lyft has a $2,500 deductible for any insurance claim. A ridiculous amount designed to put any driver off claiming on their insurance.

Should you use Lyft insurance or your own?

Lyft does offer limited insurance cover for drivers but that deductible is ridiculous. While I’m not in a position to offer specific advice, if I were driving for Lyft or Uber or whoever, I would have my own insurance cover.

Ride-sharing insurance is offered by most mainstream car insurers on most policies. It can cost anywhere from $10 extra a month upwards but is well worth the investment. Even at an extra $50 a month, it’s cheaper than the deductible and means you’re fully covered for anything that might happen.

Insurance is a complicated subject that demands more than a single page. If you have specific questions, I suggest talking to your insurer direct to get the latest, most accurate information for your specific situation.

Do you drive for Lyft? Had to claim on their insurance? Have your own insurance? Tell us about your experience below!